When one of our clients secured a $2 million retail order but lacked the working capital to fund production, they discovered how creative financing could transform their growth trajectory. As founder of GeeseCargo with extensive trade finance experience, I've witnessed how proper purchase order financing can mean the difference between capturing market opportunities and watching them disappear. The right financing approach depends on your business model, order size, and relationship with suppliers.

The best financing options for large purchase orders include purchase order financing, trade credit, supply chain financing, letters of credit, and inventory financing. Companies typically use hybrid approaches, combining 2-3 financing methods to optimize costs, flexibility, and risk. Proper financing can increase order capacity by 300-500% while maintaining healthy cash flow.

Understanding the financing landscape enables businesses to accept larger orders, negotiate better supplier terms, and grow without exhausting working capital. The most successful companies treat purchase order financing as a strategic capability rather than a reactive necessity.

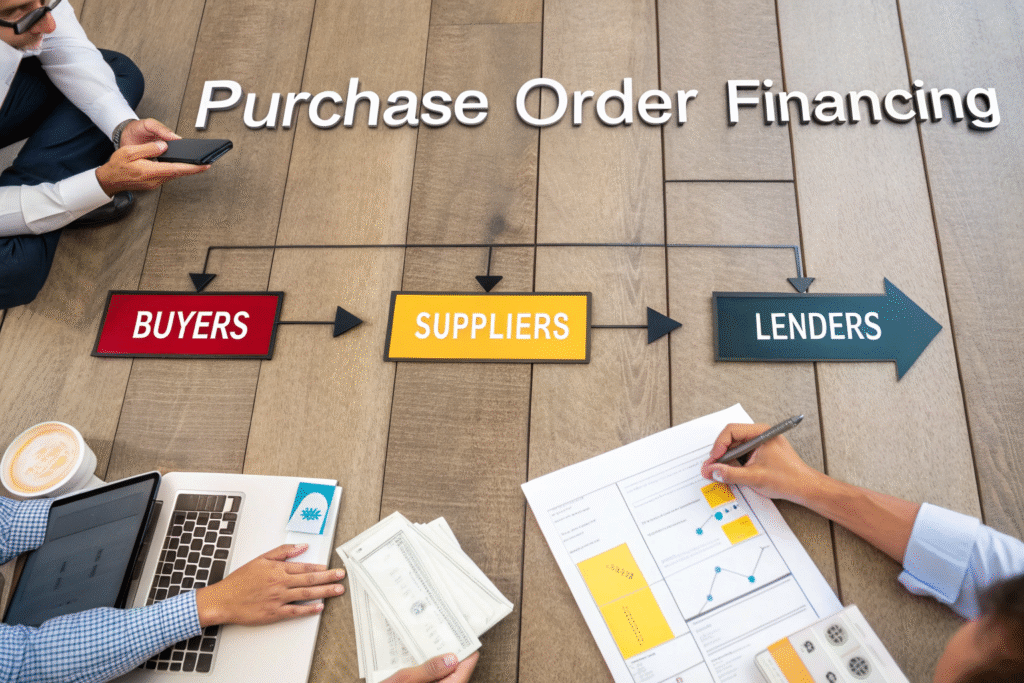

What Is Purchase Order Financing and When Does It Work Best?

PO financing provides specific funding to pay suppliers when you have confirmed customer orders but lack sufficient capital for production.

How Does the PO Financing Process Work?

Application based on confirmed customer purchase orders. Lenders evaluate the creditworthiness of your customers rather than your business, making this accessible for growing companies with strong clients but limited capital.

Direct payment to suppliers upon verification. Once approved, lenders pay your suppliers directly, ensuring production funds are used specifically for the financed orders.

Collection from end customers repays the financing. When customers pay for delivered goods, proceeds go to the lender who deducts fees and returns the balance to you.

What Types of Businesses Benefit Most from PO Financing?

Rapidly growing companies with large orders exceeding working capital. Businesses experiencing growth spikes can accept larger orders without equity dilution or long-term debt.

Seasonal businesses with fluctuating inventory needs. Companies with peak seasons can finance large inventory builds without maintaining year-round working capital for peak requirements.

Businesses with strong customers but limited operating history. Startups and growing companies can leverage their customers' credit strength to finance larger orders than their balance sheets would support.

How Can Trade Credit and Supplier Terms Reduce Financing Needs?

Negotiating extended payment terms with suppliers represents the most cost-effective financing method when available.

What Supplier Payment Terms Should You Target?

Progressive payment terms align with production milestones. Instead of 100% advance payment, negotiate 30% with order, 40% at production completion, and 30% after shipment.

Extended terms from 30 to 60-90 days improve cash flow. Each additional 30 days of supplier credit effectively provides interest-free financing for that period.

Seasonal dating or deferred payment timing. Suppliers may agree to ship goods immediately but delay payment requirements until after your peak selling season.

How Can You Negotiate Better Payment Terms?

Leverage order size and relationship history. Larger orders and proven payment history provide negotiation leverage for extended terms.

Offer compromises that benefit suppliers. Early payment discounts, longer-term commitments, or order volume guarantees can justify extended terms.

Use third-party verification to build supplier confidence. Sharing customer purchase orders or credit insurance can reassure suppliers about your ability to pay.

What Role Do Letters of Credit Play in Large Orders?

Letters of credit provide security for international transactions but also create financing opportunities through various LC types.

How Can Different LC Structures Provide Financing?

Usance (time) letters of credit create built-in payment terms. By specifying payment 30-180 days after shipment, LCs effectively provide supplier financing without direct lending.

Back-to-back LCs enable trading without capital. When you're both buying and selling goods, back-to-back LCs allow you to profit from the spread without funding the transaction.

Transferable LCs facilitate supplier payments. The ability to transfer LC proceeds to suppliers ensures they receive payment while you maintain control until performance.

What Are the Costs and Benefits of LC Financing?

Bank fees typically range from 0.75-2% of transaction value. While more expensive than trade credit, LCs provide security and enable transactions that might otherwise be impossible.

Credit utilization affects your borrowing capacity. LCs typically count against your credit lines, though some banks offer separate LC facilities.

Processing time can impact production timing. LC issuance and amendment processes may add 5-10 days to transaction timelines compared to simpler payment methods.

How Does Supply Chain Financing Optimize Working Capital?

Modern supply chain financing programs create win-win scenarios for buyers, suppliers, and financial institutions.

What Are the Main Supply Chain Financing Models?

Reverse factoring enables supplier early payment. Your bank pays suppliers early at a small discount while you pay the full amount according to original terms.

Dynamic discounting uses your cash for supplier early payment. Instead of bank funding, you pay suppliers early in exchange for discounts, effectively earning returns on excess cash.

Platform-based financing connects multiple funding sources. Technology platforms aggregate various funders to provide competitive rates for supplier early payment.

What Benefits Does Supply Chain Financing Provide?

Buyers extend payment terms without damaging supplier relationships. While you take longer to pay, suppliers can access funds immediately at reasonable rates.

Suppliers improve cash flow without taking on traditional debt. Early payment access helps suppliers fund their own operations and growth.

Financial institutions earn fees with lower risk. By leveraging the credit strength of established buyers, banks can fund suppliers with reduced credit risk.

What Alternative Financing Options Exist Beyond Traditional Methods?

Innovative financing approaches can provide solutions when traditional methods are unavailable or unsuitable.

How Can Inventory Financing Support Large Orders?

Asset-based lending uses inventory as collateral. Lenders provide funds based on the value of purchased inventory, typically advancing 50-80% of appraised value.

Warehouse receipt financing leverages stored goods. When inventory is stored in approved warehouses, receipts can be used as collateral for financing.

Floor planning finances specific inventory for resale. Common in automotive and electronics, this approach finances specific products with repayment as items sell.

What Role Does Revenue-Based Financing Play?

Repayment tied to revenue rather than fixed payments. Lenders receive a percentage of revenue until a predetermined multiple of the original advance is repaid.

Flexible structure accommodates seasonal businesses. Payments automatically adjust with revenue fluctuations, preventing cash crunches during slow periods.

Fast funding with minimal collateral requirements. Revenue-based financing typically involves less documentation and faster approval than traditional bank financing.

How Should You Structure Hybrid Financing Approaches?

Combining multiple financing methods typically provides better terms, flexibility, and risk management than relying on a single approach.

What Financing Combinations Work Best for Different Scenarios?

Large international orders often combine LCs with supply chain financing. Use LCs for supplier security and supply chain financing for extended payment terms.

Domestic orders with trusted suppliers benefit from trade credit plus inventory financing. Negotiate extended terms for what suppliers will allow, then use inventory financing for the remainder.

Rapid growth situations may use PO financing with revenue-based financing. PO financing covers supplier payments while revenue-based financing provides working capital for other expenses.

How Can You Optimize Financing Costs Across Methods?

Match financing duration to your cash conversion cycle. Use shorter-term financing like PO financing for quick turns and longer-term options for slower-moving inventory.

Layer financing based on cost and availability. Use the cheapest financing first (trade credit), then progressively more expensive options as needed.

Negotiate volume discounts with financing providers. As your financing volumes increase, negotiate better rates based on total relationship value rather than individual transactions.

What Are Common Financing Mistakes and How to Avoid Them?

Understanding frequent errors helps businesses secure better financing terms and avoid costly missteps.

What Strategic Errors Increase Financing Costs?

Over-reliance on expensive financing when cheaper options exist. Failing to negotiate trade credit or use supply chain financing can mean paying 15-30% more for capital.

Mismatched financing terms create cash flow gaps. Using 30-day financing for 90-day cash conversion cycles forces expensive refinancing or creates payment pressures.

Inadequate financing planning causes missed opportunities. Waiting until orders are received to seek financing delays production and may cause missed delivery deadlines.

What Operational Mistakes Complicate Financing?

Poor documentation slows approval and increases costs. Incomplete purchase orders, unclear supplier agreements, or missing financials delay financing and may reduce advance rates.

Inaccurate forecasting leads to financing shortages. Underestimating order sizes or timing creates last-minute financing scrambles with limited options and higher costs.

Weak supplier relationships limit financing options. Suppliers unwilling to extend terms or provide documentation make financing more difficult and expensive to arrange.

Conclusion

Financing large purchase orders requires a strategic approach that balances cost, flexibility, and risk. The most successful companies develop financing capabilities before they need them, building relationships with multiple financing sources and understanding which approaches work best for their specific business models and order characteristics.

At GeeseCargo, we've helped clients increase their order capacity by 300-600% through strategic financing approaches that match their growth stage and business model. The most effective financing strategies combine multiple methods, maintain flexibility, and evolve as businesses grow and market conditions change.

Begin your financing preparation by analyzing your historical order patterns and cash conversion cycles, then establish relationships with potential financing partners before urgent needs arise. Remember that in purchase order financing, preparation and relationships are as important as the financing terms themselves—the best financing options often go to companies who've built strong partnerships rather than those seeking emergency funding.